Innovations in Cardless Artificial Intelligence Banking: A Comprehensive Framework for Cyber Secure and Fraud Mitigation using Machine Learning Algorithms

Source: arXiv:2605.22604 · Published 2026-05-21 · By Md Israfeel

TL;DR

This paper addresses the escalating threat of fraud and cyberattacks in traditional credit/debit card banking by proposing a comprehensive framework for cardless AI banking that enhances security, convenience, and fraud mitigation. The core innovation lies in automatically generating encrypted virtual cards using AI-powered cryptography that replace physical cards, thereby reducing attack surface related to physical card loss or skimming. The framework integrates secure communication channels, homomorphic encryption for privacy-preserving data processing, and a machine learning-based fraud detection module, specifically logistic regression, to proactively identify suspicious transactions. User authorization for transaction approval is emphasized to put control in the user's hands. An end-to-end workflow is detailed from virtual card generation, encrypted transmission, merchant interaction, bank verification, fraud analysis, to transaction completion.

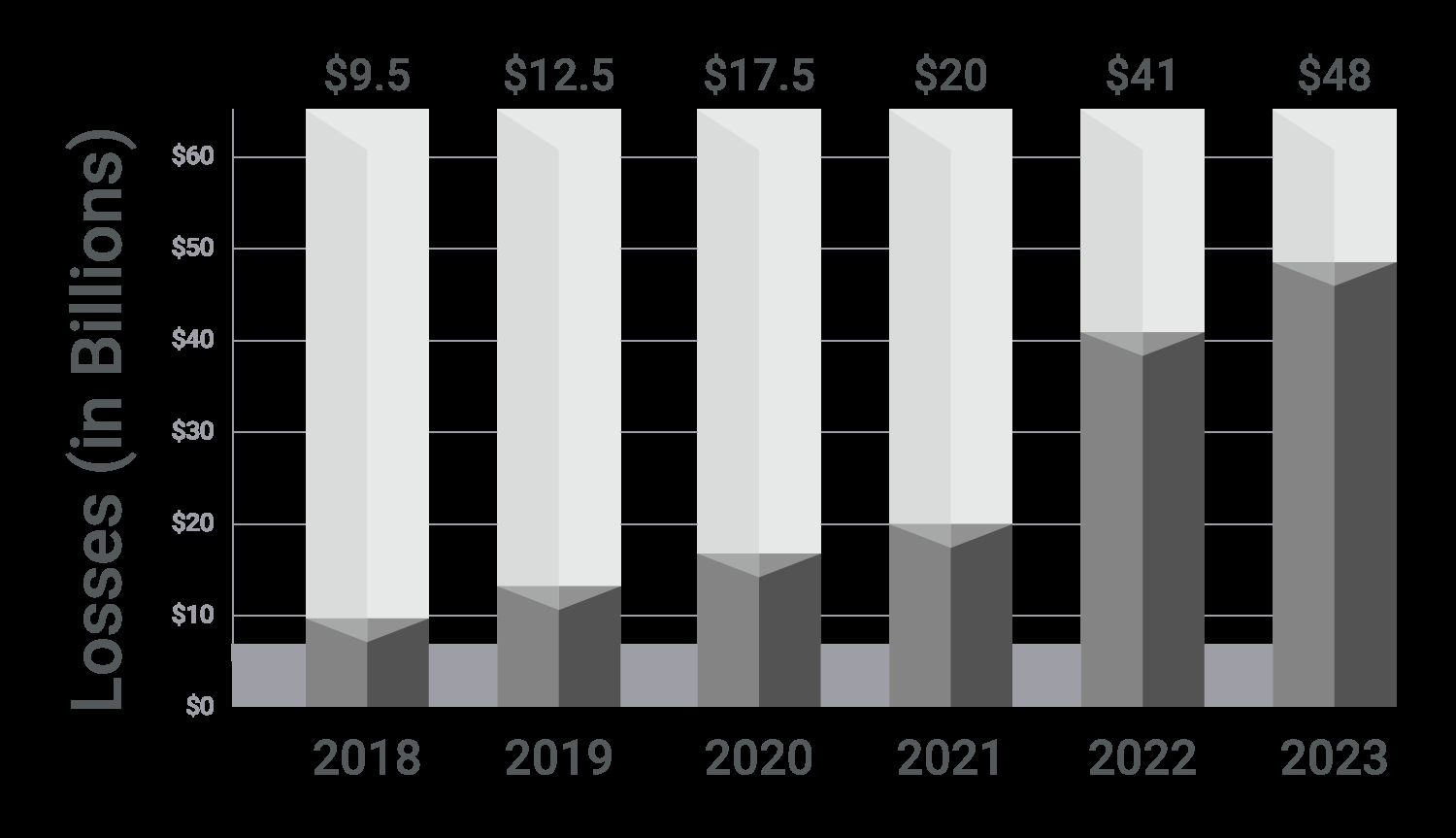

Experimental evaluation is not explicitly detailed but the paper references common fraud detection datasets (e.g., 284,807 card transactions) and situates the proposed system against rising global losses (projected $48 billion in 2023). The design leverages established machine learning and encryption methods tailored for a real-world online banking deployment scenario, emphasizing adaptability to evolving threat landscapes. Overall, the work sketches a forward-looking multi-layered approach blending cryptography, AI, and system design to construct a secure, fraud-resistant, and user-centric future of cardless digital banking.

Key findings

- Virtual cards are generated with encrypted data using homomorphic encryption, minimizing information exposure and reducing fraud risk.

- The system uses Logistic Regression-based machine learning on historical account features to detect fraudulent transactions with a fraud probability threshold of 0.5.

- The generated credit card numbers comply with ISO/IEC 7812 standard including issuer identification number (IIN), individual account identifier, and Luhn check digit.

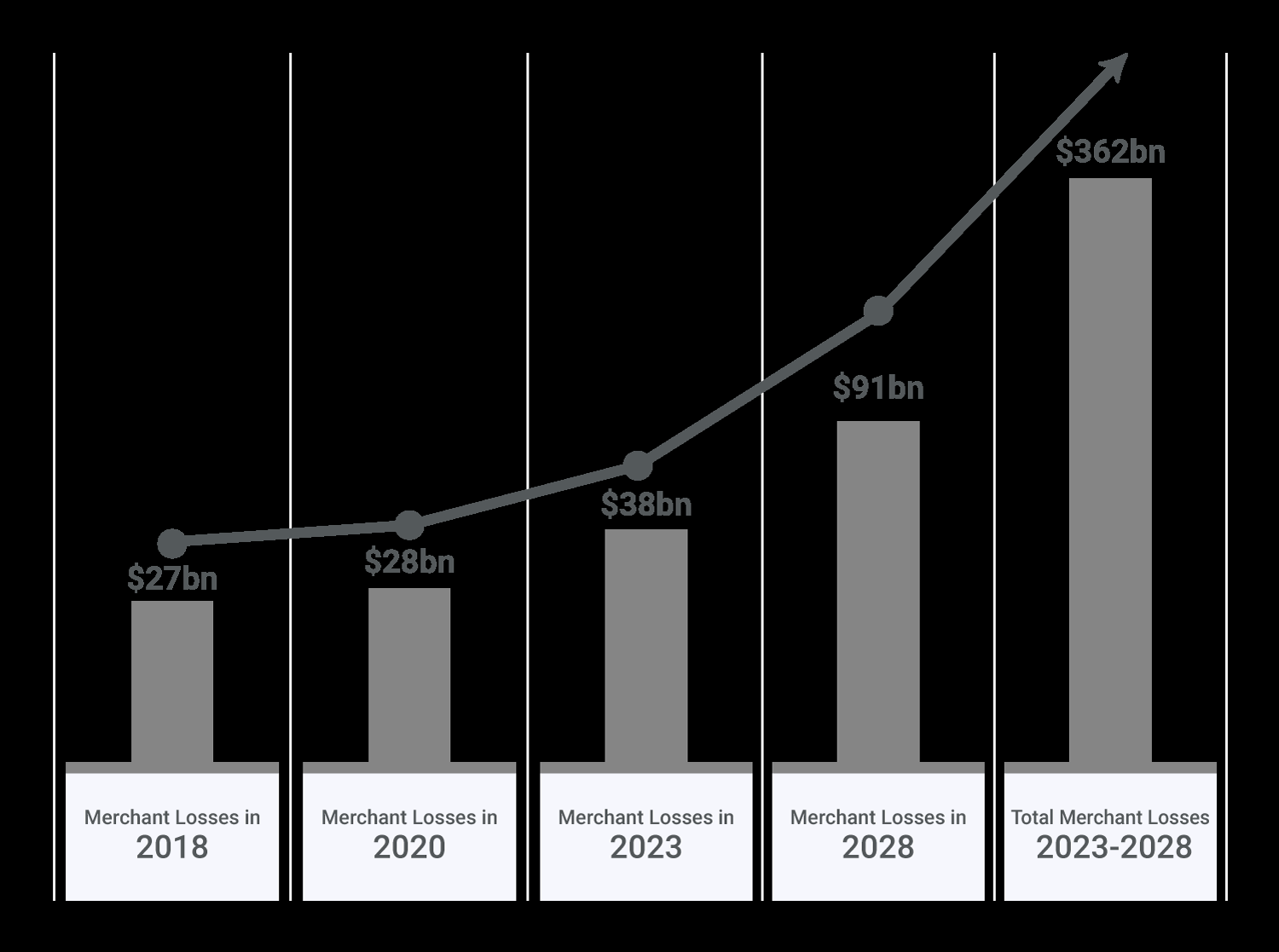

- Fraud losses in e-commerce are projected to increase from $41 million in 2022 to over $48 billion globally in 2023, underscoring urgency for improved security frameworks.

- The framework introduces a multi-phase transaction process including user authentication, virtual card generation, encrypted transmission, merchant interaction, and bank verification integrated with ML-driven fraud checks.

- Machine learning algorithms enable classifying transactions as moderate or risky in real-time based on user behavior and spending patterns.

- Continuous user authorization is required for all transactions, enhancing control and reducing unauthorized access.

- The system ensures uniqueness of virtual card numbers by checking for duplicates before issuance to prevent reuse or replay attacks.

Threat model

The adversary is a financially motivated fraudster or cybercriminal aiming to steal funds or sensitive card information through fraudulent online transactions or data breaches. They cannot break strong homomorphic encryption nor bypass multi-factor authentication without possessing valid user credentials or access devices. Insider attacks or protocol subversion are considered out of scope.

Methodology — deep read

Threat Model & Assumptions: The adversary is a cybercriminal targeting online banking transactions aiming to commit financial fraud via card theft, data breaches, phishing, or fraudulent online transactions. The attacker does not have direct access to encrypted virtual card secrets or multi-factor authentication credentials. The system assumes secure initial user authentication and trusted bank and network intermediaries.

Data: The paper references a dataset of 284,807 credit card transactions used in previous studies for machine learning fraud detection but does not elaborate on a proprietary dataset or specific splits. It acknowledges the need for diverse datasets including labeled fraud and non-fraud cases. Preprocessing is implied in feature extraction from historical account data for logistic regression.

Architecture / Algorithm: The framework consists of multiple components: an AI-enabled virtual card generator producing 16-digit card numbers compliant with ISO standards, implementing a unique identifier and Luhn check digit. The virtual card data is encrypted using homomorphic encryption to allow secure computations without decrypting privacy-sensitive data. For fraud detection, a Logistic Regression (LR) model is trained on user account features to classify transactions probabilistically, with a threshold at 0.5 for fraud. Transaction verification uses multi-factor authentication including passwords, biometrics, and device possession factors. The system includes a user authorization module demanding explicit approval on each transaction.

Training Regime: The logistic regression model is trained on historical transactional feature data; however, details such as epoch count, batch size, optimizer, or hardware specifications are not provided. Standard binary classification and thresholding techniques are used. The ML component is integrated into the transaction pipeline to enable real-time fraud scoring.

Evaluation Protocol: Quantitative evaluation with specific accuracy, precision, recall, or ROC curves is missing in the paper due to truncated content. The framework claims improved fraud detection efficacy based on cited results from prior studies. Risk is segmented into moderate vs risky transactions via behavior analytics. No explicit cross-validation or adversarial robustness tests are described.

Reproducibility: The paper does not provide code release, frozen models, or a closed dataset. Details are primarily conceptual and system-architectural. Referenced datasets in prior works are publicly known but none proprietary to this study.

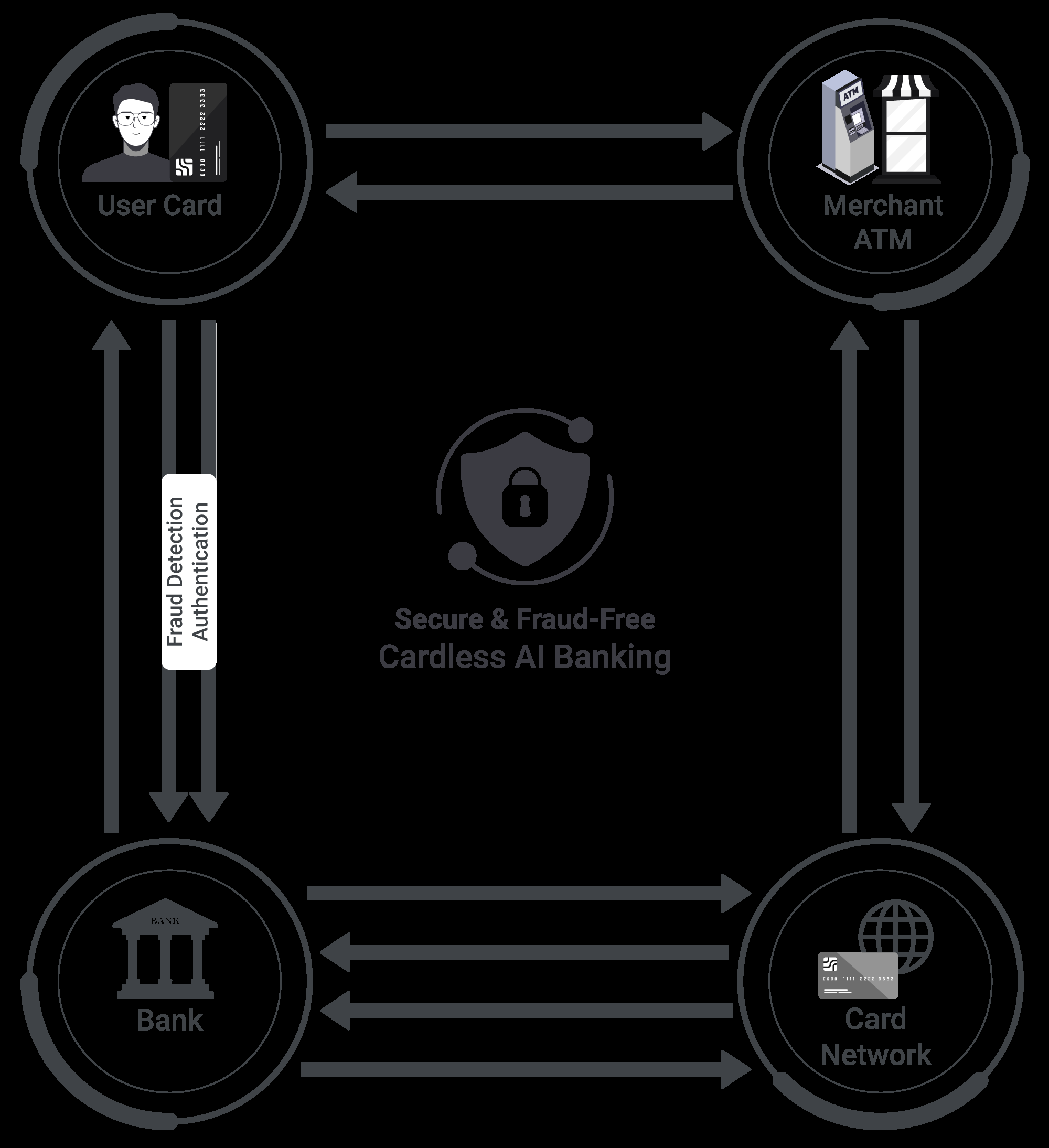

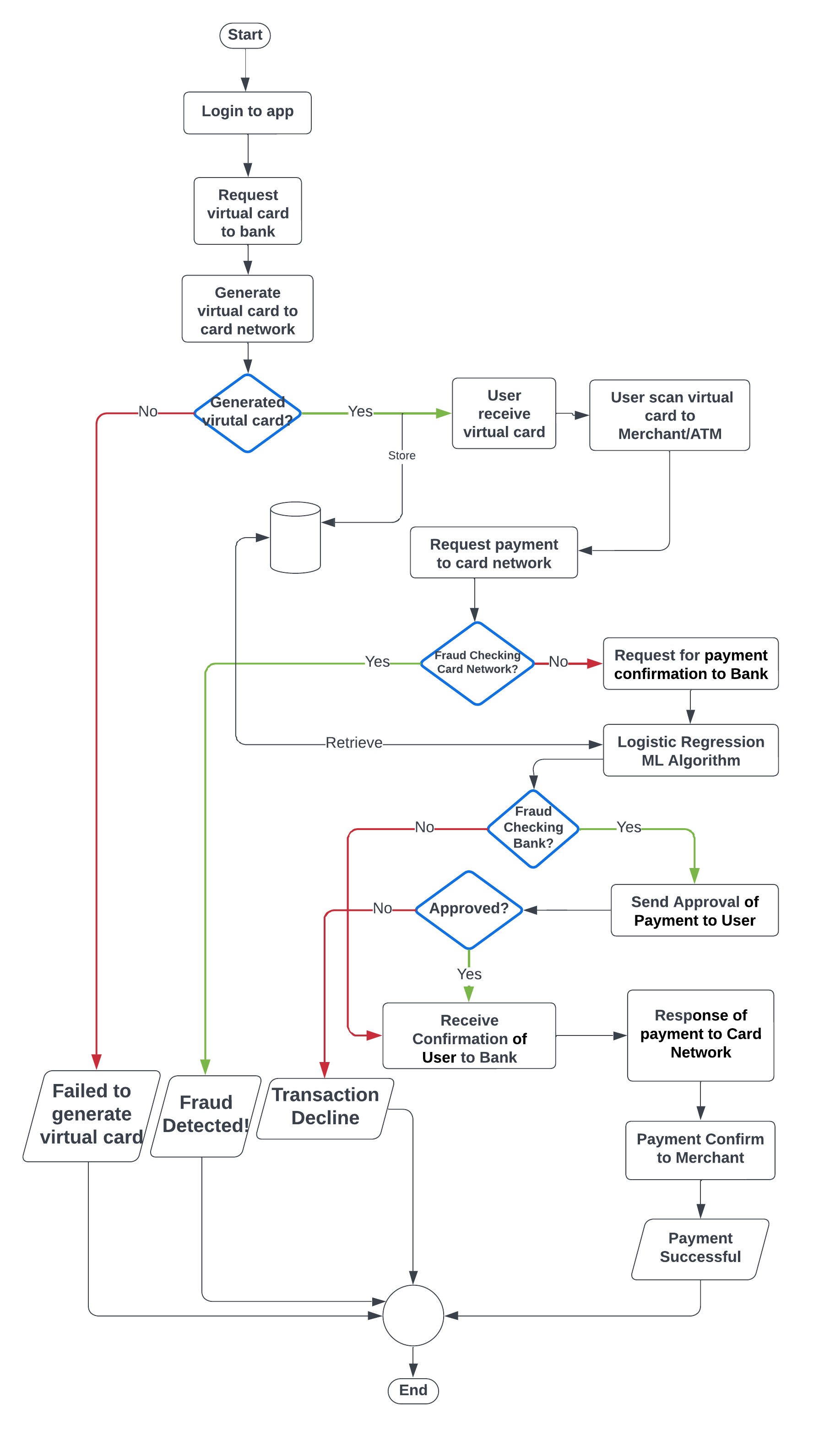

Example End-to-End Flow: A user logs into a client application, requests a virtual card generation which is created uniquely by combining an issuer identification number (IIN), a newly generated individual account identifier, and a Luhn checksum. This virtual card number is encrypted homomorphically and sent securely to the user. The user transacts at a merchant who receives only a masked card network code. The card network validates the card and calls the bank which runs fraud detection ML models and requests real-time user authorization. Upon approval, payment confirmation is sent back. The system dynamically flags suspicious transactions for further scrutiny or rejection.

Technical innovations

- Integration of homomorphic encryption with virtual card generation enables secure computations on encrypted card data without revealing sensitive information.

- Automatic generation of unique, ISO-compliant virtual card numbers with controlled usage policies (e.g., one-time or multi-use, spending limits) for cardless banking.

- Use of logistic regression machine learning on transaction historical features for real-time fraud detection integrated directly into transaction approval workflow.

- A multi-phase transaction process combining AI-based fraud detection, encrypted virtual cards, and mandatory user authorization provides a layered security model.

Datasets

- Global credit card transaction dataset — 284,807 transactions — referenced from previous studies [7]

- Online payment fraud datasets — sizes unspecified — referenced from literature [3, 25]

Baselines vs proposed

- Conventional static CVV verification: no quantitative metrics given vs proposed dynamic CVV-like virtual card scheme.

- Rule-based fraud detection systems: baseline fraud detection performance not specified vs proposed logistic regression ML approach with fraud threshold 0.5.

Figures from the paper

Figures are reproduced from the source paper for academic discussion. Original copyright: the paper authors. See arXiv:2605.22604.

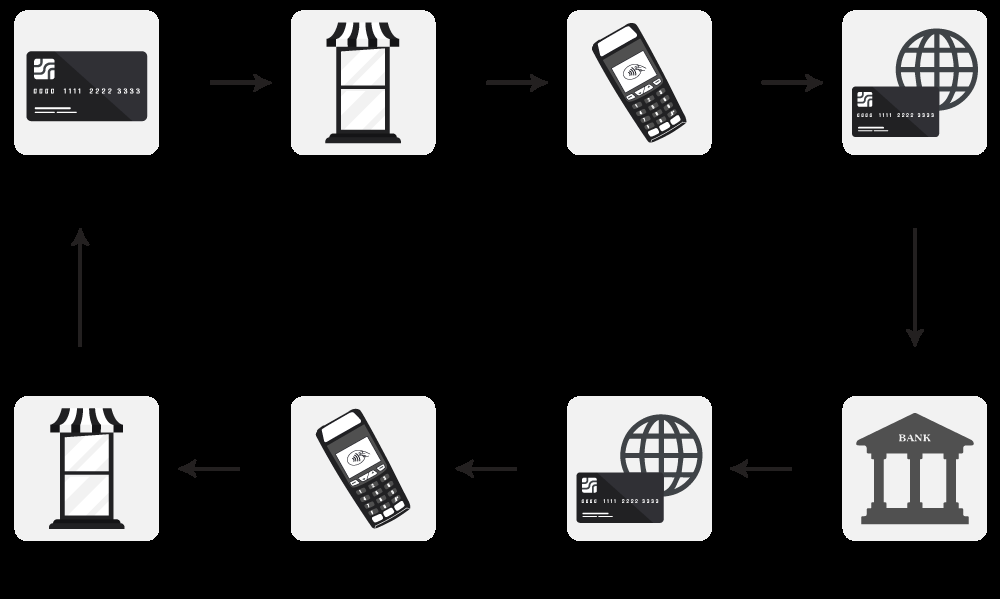

Fig 1: Current credit/debit card banking transaction overview.

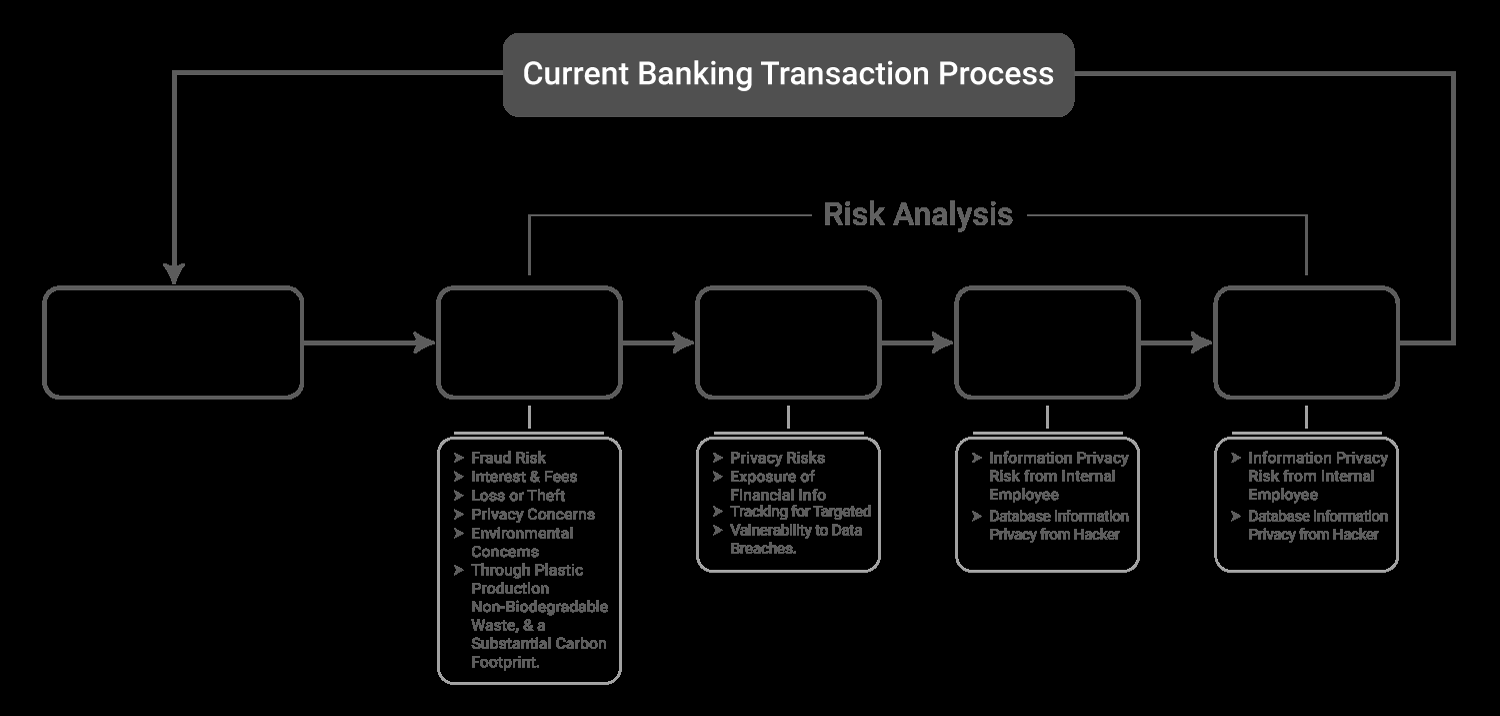

Fig 2: Risk Analysis of Current Banking Card or credit/debit System

Fig 3: Analysis and Outlook: Online Payment Fraud Trends and Market

Fig 4: The proposed banking card transaction system

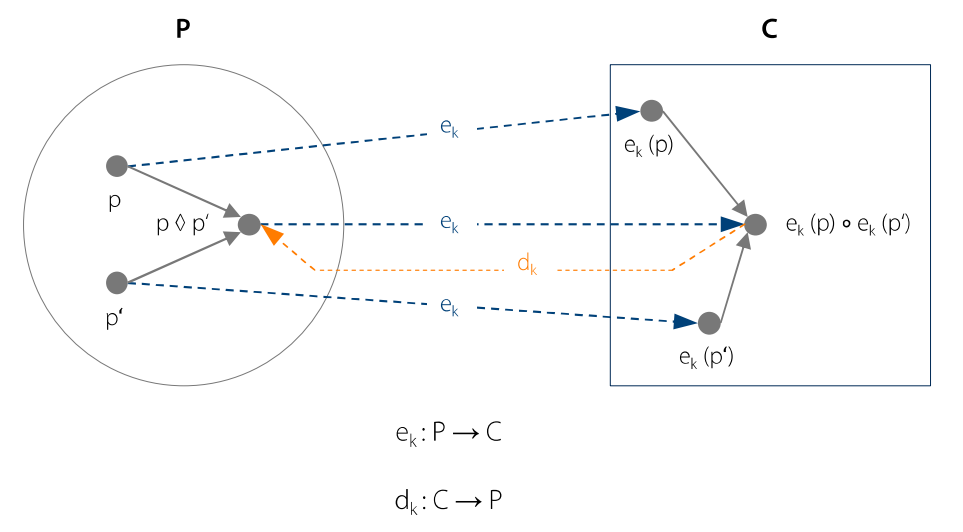

Fig 5: Homomorphism of an encryption function [35].

Fig 6: Flowchart of Bank Card Transactions Process with Machine

Fig 7: NFC to ATM, NFC to POS, or NFC to NFC

Fig 8: QR code for any smart device

Limitations

- No detailed empirical evaluation or quantitative results demonstrating fraud detection performance improvements over state-of-the-art.

- Lack of adversarial robustness testing to verify system resilience against sophisticated fraud attempts.

- No clear specification on handling distribution shifts or emerging fraud tactics beyond logistic regression adaptability.

- No publicly available codebase or dataset released for reproducibility and benchmarking.

- System assumes secure initial authentication and trusted intermediaries, not addressing insider threats explicitly.

Open questions / follow-ons

- How effective is the logistic regression model compared to more advanced or deep learning fraud detection methods in evolving attack scenarios?

- What is the performance impact and scalability of homomorphic encryption in real-time transaction processing?

- How does the system handle zero-day fraud tactics or adversarially crafted inputs targeting ML models?

- Can user experience be optimized to avoid friction from continuous authorization while maintaining security?

Why it matters for bot defense

For bot-defense and CAPTCHA practitioners, this research offers insights into constructing layered fraud defense mechanisms combining cryptographic protections with machine learning-based anomaly detection. The framework’s emphasis on AI-driven dynamic virtual cards and mandatory user authorization aligns with trends toward minimizing attack surfaces exposed to automated bots. However, the paper does not directly address bot detection techniques or CAPTCHA integration. Practitioners could consider leveraging similar ML-based fraud risk scoring in conjunction with bot detection triggers or CAPTCHA challenges to differentiate between legitimate users and scripted attacks. The adoption of encrypted transaction tokens may reduce traditional attack vectors exploited by bots, but validating user intent remains critical. Overall, the study underscores the importance of holistic, adaptive defenses in online financial services but leaves room for integrating specialized bot-defense mechanisms within this broader architecture.

Cite

@article{arxiv2605_22604,

title={ Innovations in Cardless Artificial Intelligence Banking: A Comprehensive Framework for Cyber Secure and Fraud Mitigation using Machine Learning Algorithms },

author={ Md Israfeel },

journal={arXiv preprint arXiv:2605.22604},

year={ 2026 },

url={https://arxiv.org/abs/2605.22604}

}